Ito Integral Geometric Brownian Motion

This expression has some advantages over the ones. This is by enhancing the Laplace transform ansatz of Yor 1992 with complex analytic methods which is the main methodological contribution of the paper.

Stochastic Calculus Main Results

Calculus should be used It.

Ito integral geometric brownian motion. BROWNIAN MOTION AND ITOS FORMULA 3 The standard form of a probability triple is FP where is the set of all possible outcomes called the sample space and Fis the collection of events which are subsets of to which we can assign a probability. Brownian motion A process Wt is called a Brownian motion or Wiener process if 1. Note that a collection of random variables X.

Calculus is introduced in the next cahpter of the book. It will be apparent that the. BROWNIAN MOTION AND ITO CALCULUS 3ˆ Definition 16.

6182016 It introduces concepts such as conditional expectation with respect to a sigma-algebra filtrations adapted processes Brownian motion BM martingales quadratic variation and covariation the It. Lets use that and verify if your solution is correct. We will then briey outline the way an Ito integral is deflned.

However our goal is rather modest. Itos Rule Proposition 12 If f fx is a twice differentiable function with a continuous second deriva-tive f00x then dfBt f0BtdBt 1 2 f00Btdt differential form 6 fBt fB0 Z t 0 f0BsdBs 1 2 Z t 0. The Ito integral leads to a nice Ito calculus so as to generalize 1 and 3.

μ t x t μ. Brownian Motion and Itos Lemma 1 Introduction 2 Geometric Brownian Motion 3 Itos Product Rule 4 Some Properties of the Stochastic Integral 5 Correlated Stock Prices 6 The Ornstein-Uhlenbeck Process. This exerice should rely only on basic brownian motion properties in particular no It.

This is aˆ vast subject. Let the stock price S follows the geometric brownian motion. This paper is about the probability law of the integral of geometric Brownian motion over a finite time interval.

782016 There are two types of integrals involving Brownian motion time integral and itos integral. D S S μ d t σ d z. This form is preferable because of its similarity to Taylors formula.

Naively integrating the second equation above over time t gives. T f t X t d t x f t X t R t d W t d B t 1 2 x x f t X t R t 2 d t. Ive always preferred the similar form of Itos Lemma present on wikipedia.

We will develop this the-ory only generally enough for later applications. Stochastic Integration and Itos Formula In this chapter we discuss Itos theory of stochastic integration. A partial differential equation is derived for the Laplace transform of the law of the reciprocal integral and is shown to yield an expression for the density of the distribution.

Integral with respect to BM Its lemma Girsanov theorem for a single BM and geometric Brownian motion GBM model. Since the above formula is simply shorthand for an integral formula we can write this as. Geometric Brownian motion According to Levy s representation theorem quoted at the beginning of the last lecture every continuoustime martingale with continuous paths and finite quadratic variation is a timechanged Brownian motion.

Where d z is a wiener process. T WtWs follows a normal distribution with mean zero and variance σ2 ts where σ is a positive constant.

This paper studies the law of any power of the integral of geometric Brownian motion over any finite time interval. Begineqnarray logSt - logS0 leftmu - frac12 sigma2 rightt sigma Bt endeqnarray. T Wt Ws and Wr are independet that is inde-pendent increments.

As its main results two integral representations for this law are derived. Here the integral is a time integral which is just an ordinary Lebesgue integral. 33 223241 2001 Printed in Northern Ireland Applied Probability Trust 2001 THE INTEGRAL OF GEOMETRIC BROWNIAN MOTION DANIEL DUFRESNE Universit.

D x t x t μ d t x t σ δ t d Z t. THE ITO CALCULUSˆ 1. The probability of.

L n S T S 0 μ T 0 σ z T z 0. The σ-fields G i are independent if n N i 1i n Iwith i j 6 i l for j6 1 and for all G i j-measurable random variables X i j j 1nwe have. 8122019 Viewed 238 times.

Using as a simplification the variable change s tu one has that t0Bsds tUt where Ut 10Btudu. The random variables X i 1X i n are independent. σ t x t σ δ t f x F x ln.

We will discuss stochastic integrals with respect to a Brownian motion and more generally with re-. 0 T 1 S d S 0 T μ d t 0 T σ d z. We will do that mostly by focusing hard on one example in which we integrate Brownian motion with respect to Brownian motion.

In the case where d M R t d W t is is an integral with respect to brownian motion so d M t R t 2 d t is is convenient to simplify further. Where Z t is brownian motion. D S μ S d t σ S d z.

For Brownian motion Wt let Ft σWss t t 01. The integral itself is also a random variable as it depends on the path of brownian motion. We start with your process.

It is a standard Brownian motion with a drift term. It is summarized by Itos Rule. Let G i i F i I.

GBM is used to.

Pdf Study On Geometric Brownian Motion With Applications

Stochastic Calculus Main Results

Outline Geometric Brownian Motion Stratonovich And Ito Models Ppt Video Online Download

Stochastic Calculus Main Results

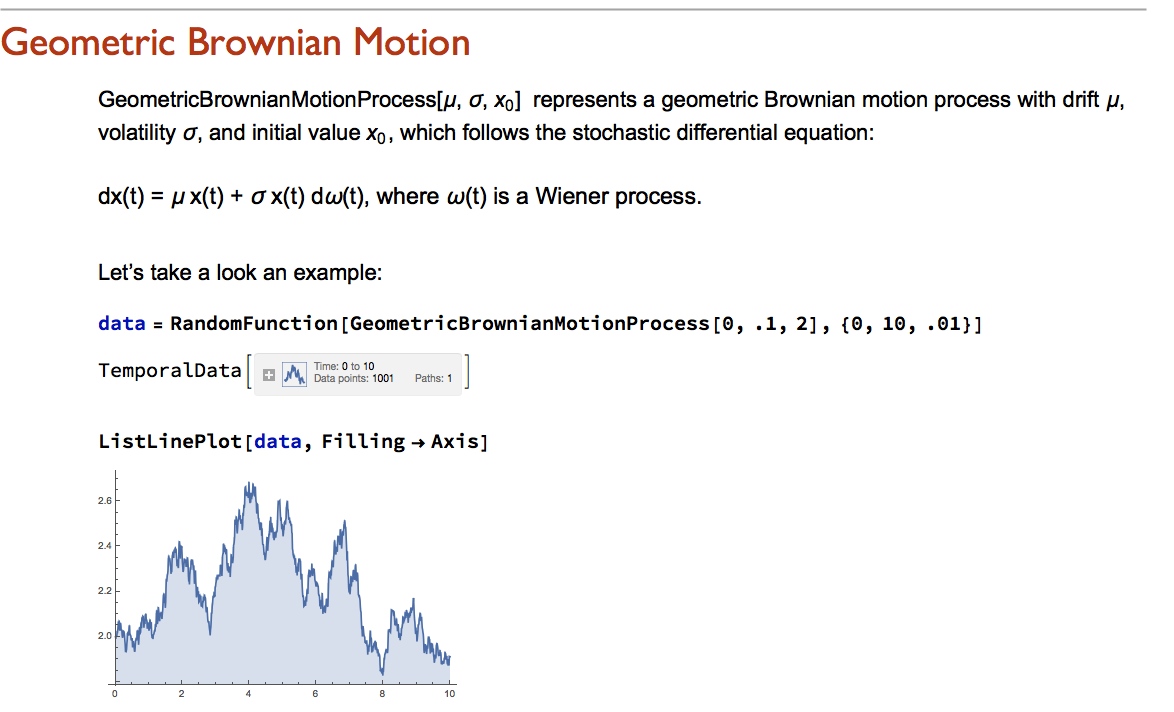

Stochastic Calculus In Mathematica

Komentar

Posting Komentar