Ito Process Brownian Motion

Stochastic Processes as Measures on Path Space 9 25. First for Ito processes and Brownian motion.

Random Walk Brownian Motion And Sdes Ppt Download

Markov Processes 17 35.

Ito process brownian motion. Construction of Brownian Motion 13 32. Ask Question Asked 8 days ago. Brownian motion and It.

Using as a simplification the variable change stu one has that int_0t B_s dstU_t where U_tint_01 B_tudu. It is a standard Brownian motion with a drift term. Brownian Motion as a Markov Process 18 36.

This is Brownian motion with an instantaneous drift at and an instantaneous variance b2 t. For two Brownian motions which are not independent we would like to describe the dependence of the two processes - this is done by introducing the so-called correlation coefficient varrho. So let me explain what the meaning of this is.

It is an important example of stochastic processes satisfying a stochastic differential equation. Calculus is introduced in the next cahpter of the book. In particular it is used in mathematical finance to model stock prices in the BlackScholes model.

This importance has its origin in the universal properties of Brownian motion which appear as the continuous scaling limit of many simple processes. Apply Itos lemma Theorem 20 on p. Itos Formula for Brownian Motion.

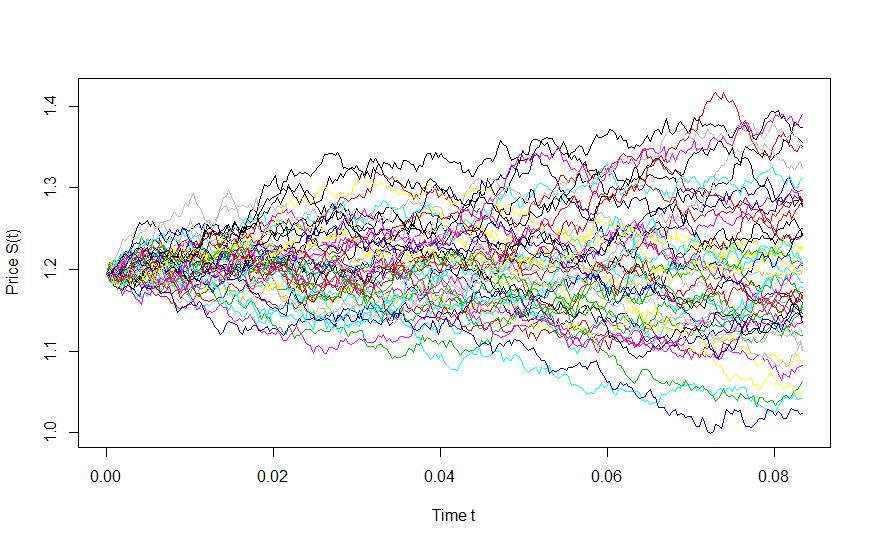

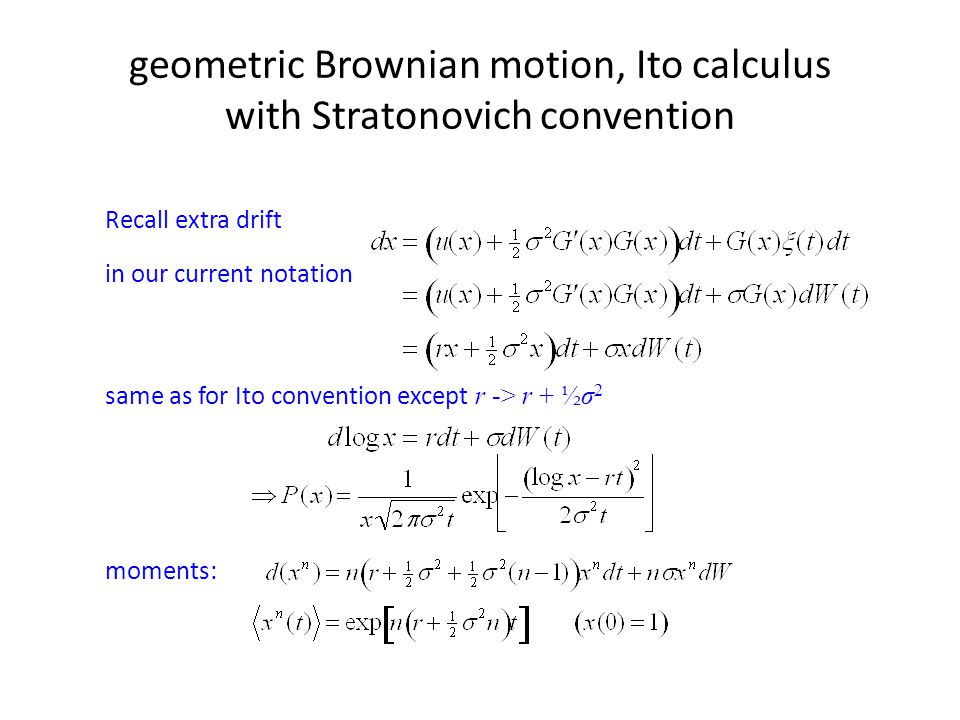

3302003 A geometric Brownian motion is a continuous-time stochastic process in which the logarithm of the randomly varying quantity follows a Brownian motion with drift. 3The process fW tg. Geometric Brownian motion According to Levy s representation theorem quoted at the beginning of the last lecture every continuoustime martingale with continuous paths and finite quadratic variation is a timechanged Brownian motion.

2With probability 1 the function tW tis continuous in t. There is one important fact about Brownian motion which is needed in order to understand why the process S t eBte 22t 1 satis es the stochastic di erential equation dS Sdt SdB. The Law of Iterated Logarithms 16 34.

682019 The derivation shows that a function of a Ito process is also a Ito process and the randomness of the two processes is the same and comes from the same underlying Brownian motion. Those processes are the base of Stochastic integration and are therefore widely used in financial mathematics and stochastic calculus. Active 2 days ago.

Ito Process continued A shorthanda is the following stochastic differential equation for the Ito differential dXt dXt aXtt dt bXtt dWt. 572021 Bounding Brownian motion and an Ito process simultaneously. Ito process consists in fact of two parts.

DU Z dY Y dZ dY dZ ZY adt bdWY Y Zf dt gdWZ Y Zadt bdWYf dt gdWZ U a f bgρ dt UbdWY UgdWZ. Calculus Brownian motion is a continuous analogue of simple random walks as described in the previous part which is very important in many practical applications. B t 2 0 t 2 B s d B s 0 t s.

This exerice should rely only on basic brownian motion properties in particular no It. A standard one-dimensional Wiener process also called Brownian motion is a stochastic process fW tg t 0 indexed by nonnegative real numbers twith the following properties. Brownian Motion 11 31.

2 The crucial fact about Brownian motion which we need is dB2 dt. Reflection Principle 19 37. This is an Ito drift-diffusion process.

Viewed 116 times 5. S formula where the usual second order. 1 begingroup The bounty expires in 2 days.

I and Goodman indicates one way to construct a Brownian motion. Itos Formula for Brownian Motion. Begineqnarray logSt - logS0 leftmu - frac12 sigma2 rightt sigma Bt endeqnarray.

If varrho0 then the Brownian motions are independent otherwise they are not. Consider the Ito process U YZ. An Ito process is a type of stochastic process described by Japanese mathematician Kiyoshi It which can be written as the sum of the integral of a process over time and of another process over a Brownian motion.

48 Or simply dXt at dt bt dWt. No matter how much youd zoom in it will look similar. Consider a d-dimensional Brownian motion X X 1X d and a function F which belongs locally to the Sobolev space W 12.

Yuh-Dauh Lyuu National Taiwan University Page 514. Ito process is a continuous-time trajectory with random evolution so non-smooth and very kinky - also has a fractal look. 1 W 0 0.

Since the above formula is simply shorthand for an integral formula we can write this as. We prove an extension of It. THE ITO CALCULUSˆ 1.

Often Itos formula is used for computing the dynamic of a function of a Brownian motion for example of B t 2 where applying the usual formula we get. Brownian Motion and Itos Lemma 1 Introduction 2 Geometric Brownian Motion 3 Itos Product Rule 4 Some Properties of the Stochastic Integral 5 Correlated Stock Prices 6 The Ornstein-Uhlenbeck Process. X is a martingale if at 0 Theorem 17 on p.

Calculus should be used It. The drift part deterministic evolution and the diffusion part where all the kinkiness and fractalness comes. But why we can do that.

Answers to this question are eligible for a 50 reputation bounty. Product of Geometric Brownian Motion Processes Let dYY adt bdWY dZZ f dt gdWZ. Regularity of Brownian Motion 14 33.

Geometric Brownian Motion An Overview Sciencedirect Topics

How To Use Brownian Motion In Trading Forex Trading 2 0

Outline Geometric Brownian Motion Stratonovich And Ito Models Ppt Video Online Download

Graphical Illustration Of The Bessel Process A Trajectory Of A Download Scientific Diagram

Computer Simulation Of Brownian Motion With Decay Employing 1000 N Download Scientific Diagram

Komentar

Posting Komentar