Ito Lemma Stochastic Differential Equation

Suppose that a function depends on the n variables xX2 x. Itos Lemma is crucial in deriving differential equations for the value of derivative securities such as stock options.

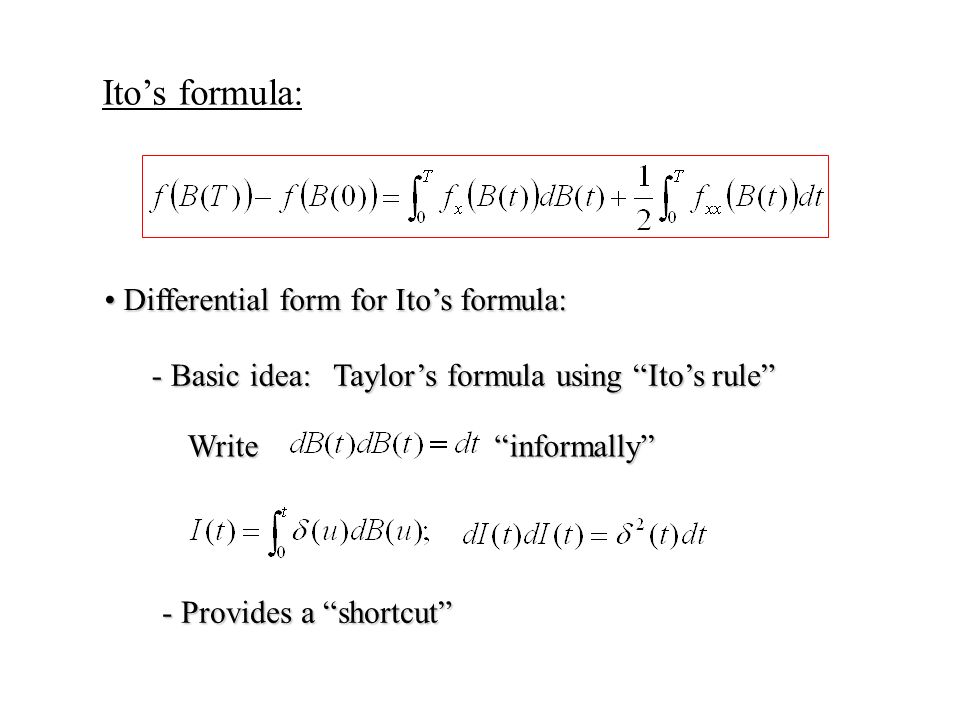

Theoryapplication Discrete Continuous Stochastic Differential Equations Ito S Formula Derivation Of The Black Scholes Equation Markov Processes Ppt Download

24102018 Here I briefly present the derivation for the Fokker-Planck equation from a stochastic differential equation.

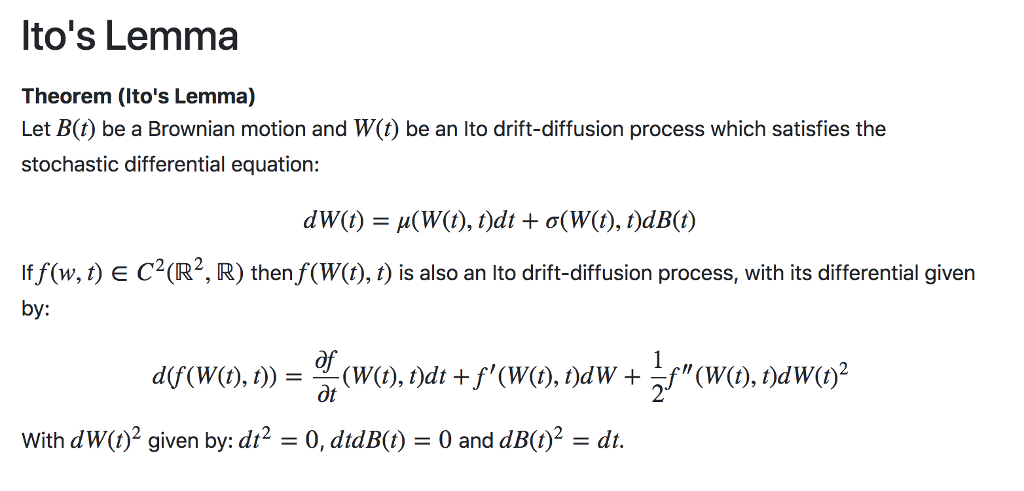

Ito lemma stochastic differential equation. 3032019 Assuming you are talking about unconditional expectation in general you have. Itos Lemma Theorem Itos Lemma Let Bt be a Brownian motion and Wt be an Ito drift-diffusion process which satisfies the stochastic differential equation. For simplicity lets assume that t 1 so that fB 1 fB 0 Z 1 0 f0B sdB s 1 2 Z 1 0 f00B.

Itos Lemma gives the answer. Itos Lemma Theorem 31 Itos Lemma I. Equation 1 becomes Itos formulaˆ duudx 1 2 udx2 2 This equation is exact.

Then the process Yt gtXt is again an Ito process whose kth componentˆ k. SystemdXtbtXtdttXtdUt612 whereUtisp-dimensional Brownian motion. DX_t bX_t 1dt 2 sqrtX_tdW_t I then am told to let Y_t sqrtX_t and thus derive the Ito stochastic differential equation dY_t AY_t dt BY_tdW_t and to then determine AY_t BY_t.

Finally taking the exponential of this equation gives. Suppose further that follows an Ito process with instantaneous drift a and instantaneous variance bj 1. As discussed earlier the Ito interpretation of this equation is.

In standard calculus the differential of the composition of functions latex fx xtfg000000 satisfies latex dfxtfprimextdxtfg000000. Then Itos lemma gives d B2 t dt 2B tdB t This formula leads to the following integration formula Z t t 0 B dB 1 2 Z t t 0 d B2 Z t t 0 d B2 t tB t 2 0 2 0 2. Itos lemma for the process followed by a function of several stochastic variables.

14112016 begingroup bf93. For other versions see 1. Itos lemma also named Itos formula is a fundamental concepts of the stochastic differential equations.

Your mistake is the following in fact using Its lemma you should find out that. 4 pftfSa fS b. Given the stochastic process dxaxtdtbxtdW_t where W_t is a Wiener process.

The third-order and higher order terms are zero. Let St be a function in t satisfies the follows stochastic differential equation. The deterministic and stochastic components of dC are given by.

Now I am attempting to model a Stochastic Damped Harmonic Oscillator with a random driven force which I found in a book called Modeling with Ito Stochastic Differential Equations. 2012010 Itos lemma otherwise known as the Ito formula expresses functions of stochastic processes in terms of stochastic integrals. DZ_tZ_tdt the solution of this deterministic ode is Cet so using Z_0x2y2 you can identify C.

By Ito lemma for any twice. 3 Applications of Itos Lemma Let fB t B2 t. Rnpsatisfy conditions 521 522 and.

There are different important versions of the Itos lemma here we only present the Itos lemma with space and time variables. E X t E e W t e E W t 1 2 Var W t which yields. Answered Mar 31 19 at 1952.

The formula above can also be written in di erential form as dfB t f0B tdB t 1 2 f00B tdt. We also assume that the distri- bution ofX0is known and independent ofUt. So we have an Ito Stochastic Differential Equation with b as a constant.

15 Solving Stochastic Differential Equations - YouTube. D xt vt dt Eq. 2 d Mt -k xt - b vt dt Sqrt2 gamma2 lamda d Wt.

Then for every t fB t fB 0 Z t 0 f0B sdB s 1 2 Z t 0 f00B sds. Hence E X 2 e. Letˆ gtx g 1txg ptxp 2N be a C2 map from 01 Rn into Rp.

Theorem - The general Ito formulaˆ Let Xt X0 Zt 0 us ds Zt 0 vs dBs be an n-dimensional Ito process. Financial Economics Itos Formulaˆ Stochastic CalculusItos Formulaˆ In stochastic calculus one must also keep the second-order terms. 2512010 Recall that Itos lemma expresses a twice differentiable function latex ffg000000 applied to a continuous semimartingale latex Xfg000000 in terms of stochastic integrals according to the following formula latex displaystyle fX fX_0int fprimeXdX frac12int fprimeprimeXdX.

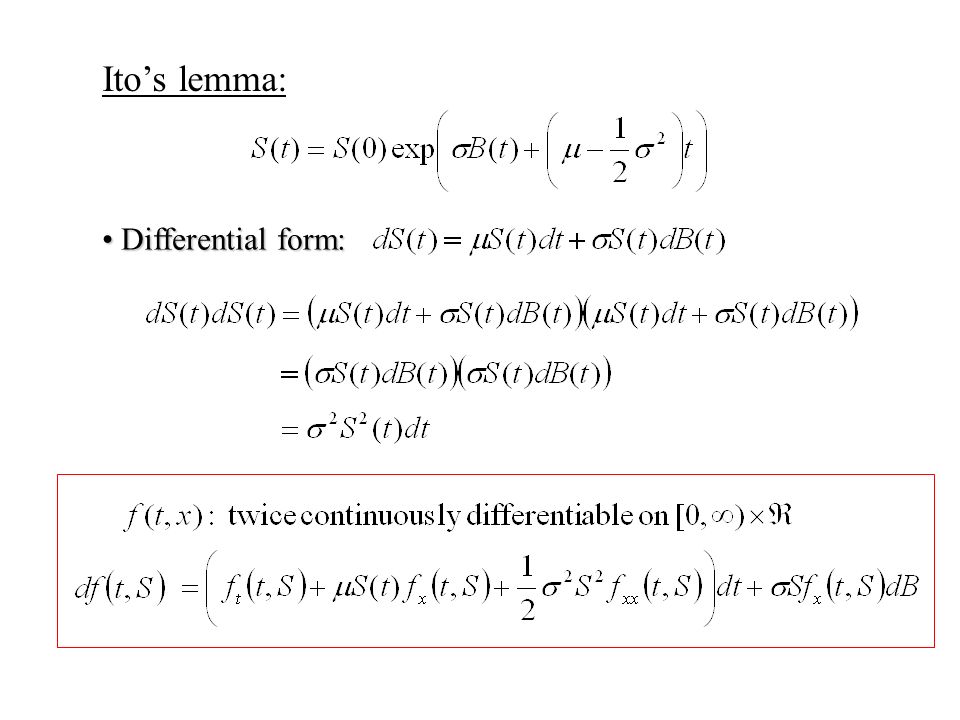

Here is the model. E X t e 1 2 t. S t S 0 exp μ 1 2 σ 2 t σ B t This is the solution the stochastic differential equation.

Begineqnarray dWt muWttdt sigmaWttdBt endeqnarray. Suppose fis a C2 function and B t is a standard Brownian motion. Fg000000 1 In this form the.

N that is dxi idt bidzi. 15 Solving Stochastic Differential Equations. Equation 10 is called Itos lemma and gives us the correct expression for calculating di erentials of composite functions which depend on Brownian processes.

Theoryapplication Discrete Continuous Stochastic Differential Equations Ito S Formula Derivation Of The Black Scholes Equation Markov Processes Ppt Download

Worked Examples Of Applying Ito S Lemma Quantitative Finance Stack Exchange

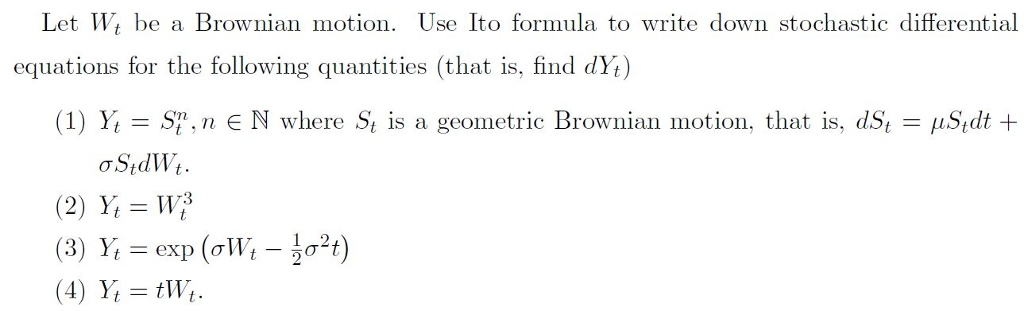

Solved Let Wi Be A Brownian Motion Use Ito Formula To Wr Chegg Com

Solved Lto S Lemma Theorem Lto S Lemma Let B T Be A Br Chegg Com

Checking A Solution To The Linear Homogeneous Sde Mathematics Stack Exchange

Komentar

Posting Komentar